Article 12 Summary: Digital payments in India: A $10Tn Opportunity

Article by BCG & PhonePe Pulse

Number of pages: 31

Summary:

India has undergone a significant digital payments transformation in the last five years, with 40% of payments being digital, contributing to a $3 trillion digital payment market. The growth has been fueled by expanding digital infrastructure, UPI-led migration, pandemic-induced shifts in customer preferences, and fintech innovations. Despite this, certain market segments remain underpenetrated, with the next growth wave expected from Tier 3-6 cities. Factors like merchant acceptance expansion, value chain digitization, and financial services marketplaces in underpenetrated areas will drive rapid digital payment growth.

Embedded payments through 5G and IoT, along with the introduction of India's Digital Rupee, are anticipated to further boost the digital payments landscape. The market is poised to triple to $10 trillion by 2026, constituting nearly 65% of all payments. Merchant payments, particularly offline, are predicted to surpass person-to-person transfers. As digital payments become integrated into commerce, there's a shift towards embedded finance, enabling broader access to credit for small merchants.

While thin margins pose a challenge for payment players, they are leveraging their customer base and data to diversify revenue streams, including lending and investment facilitation. This trend is leading to the emergence of super app ecosystems. To unlock the $10 trillion opportunity, building customer trust, addressing fraud management, simplifying digital onboarding and KYC, easing tech infrastructure strain, ensuring better economics for payment players, and strengthening digital infrastructure are crucial enablers.

Explosion of digital payments:

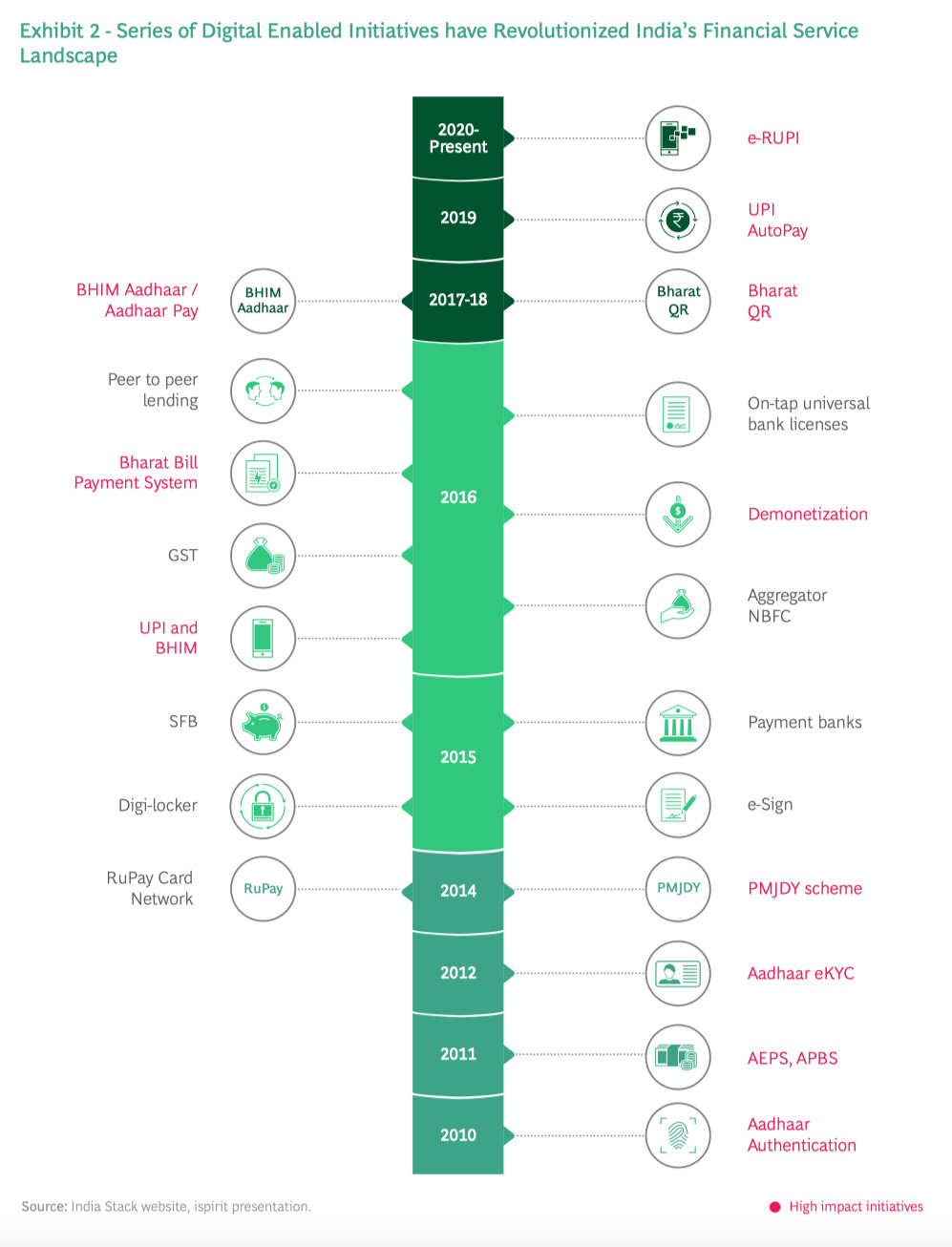

The Indian payment landscape has experienced a significant shift, with 2 out of 5 transactions, amounting to around $3 trillion, being digital. The growth is attributed to the Jan Dhan Yojana program, which facilitated bank account penetration with 440 million accounts, 1.25 billion Aadhaar-based unique identification numbers, over a billion mobile devices, and widespread low-cost internet. The JAM trinity (Jan Dhan, Aadhaar, Mobile) has laid the foundation for this growth. The India Stack infrastructure, including UPI, Bharat Bill Payment System (BBPS), and National Electronic Toll Collection (NETC), has played a crucial role, along with QR code standardization, simplifying merchant acceptance.

Accelerated migration to digital led by UPI

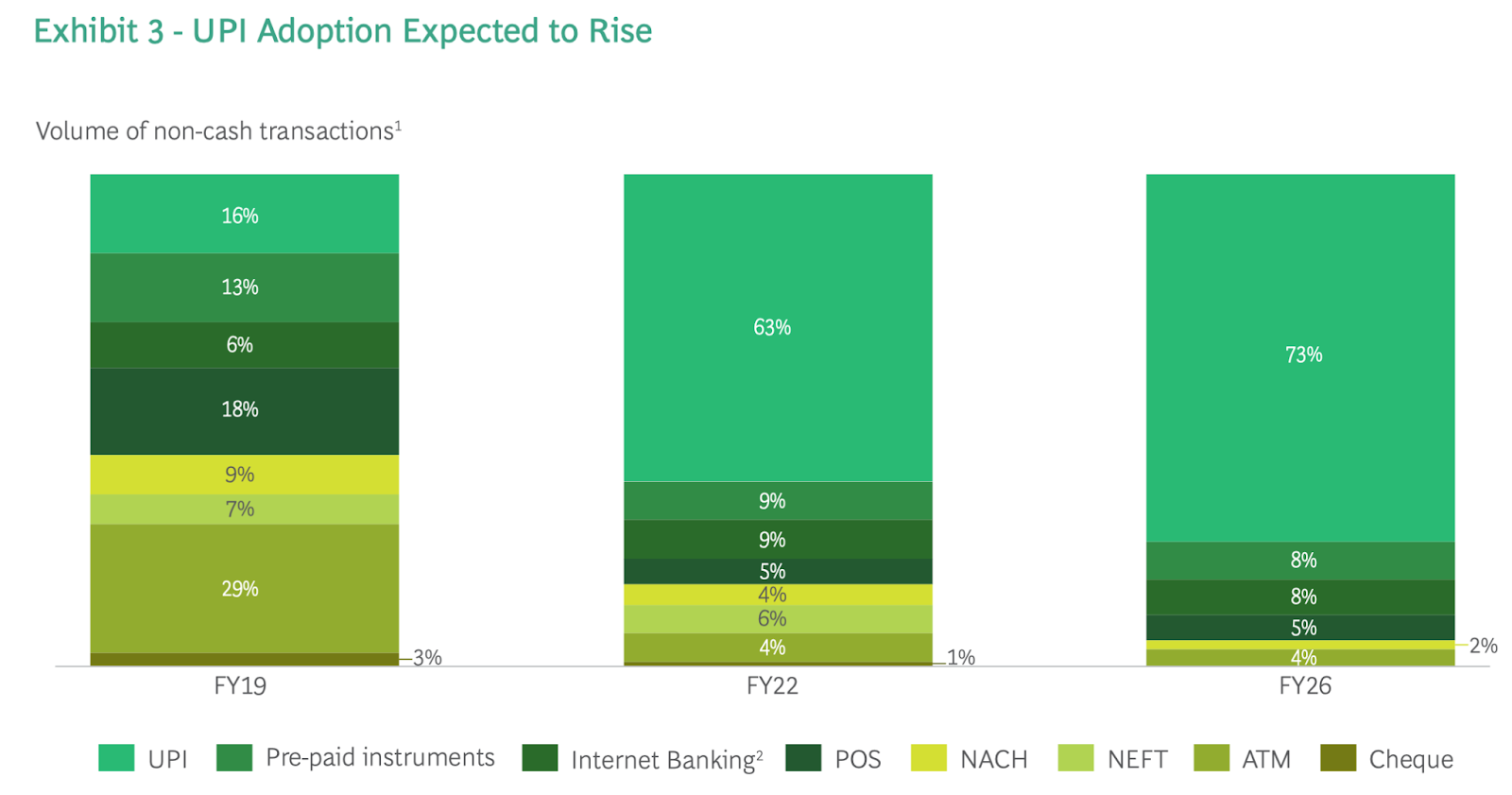

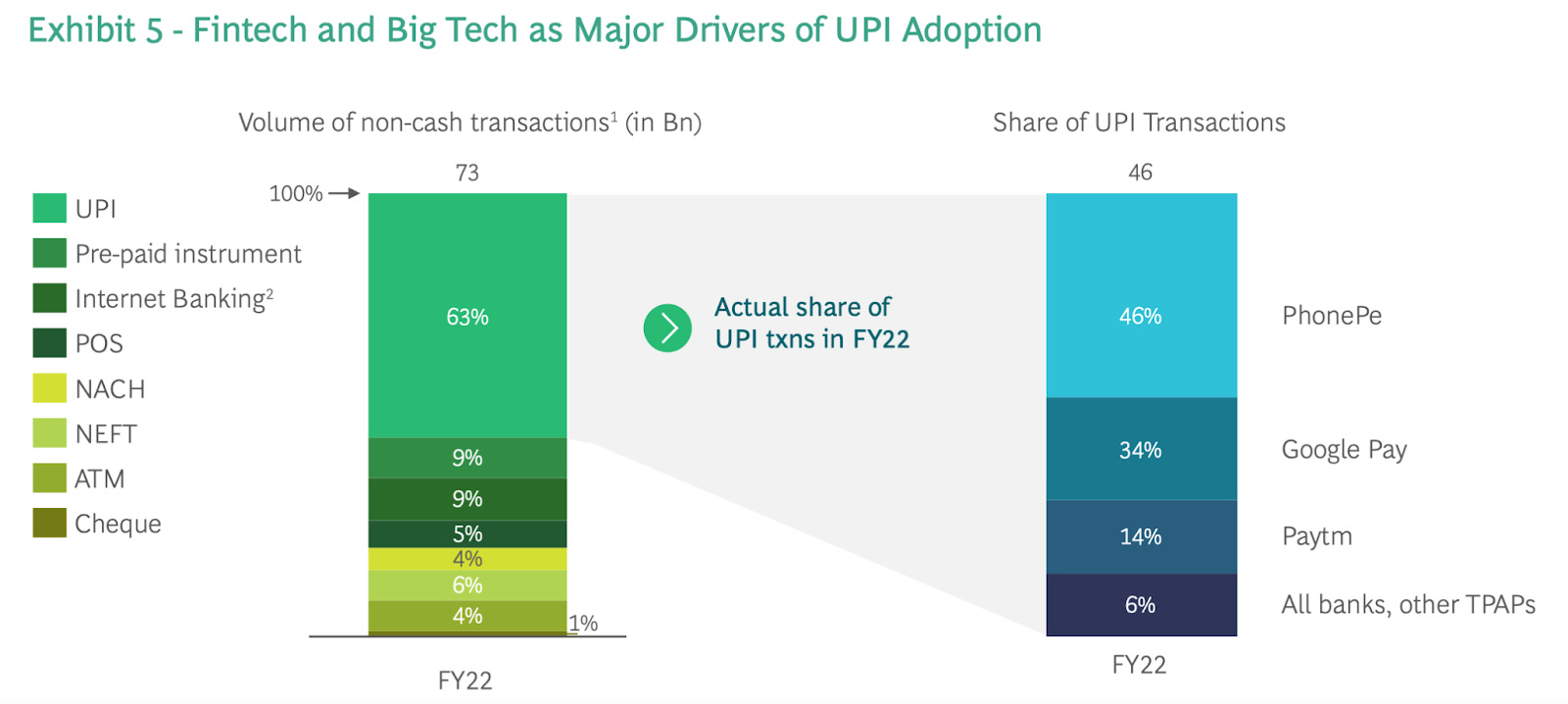

Private players, such as third-party application providers (TPAPs) and wallets, adopting these protocols and public goods have contributed to the success of digital payments as a public-private partnership (PPP). UPI, in particular, has accelerated the migration to digital, witnessing a 9x increase in transaction volume over the past three years, reaching about 46 billion transactions in FY22. UPI transactions, directly linked to bank accounts without wallet top-ups, are approximately 9x credit and debit card transactions in volume. The growth trajectory suggests that UPI is expected to drive around 75% of total digital transaction volumes in the next five years.

Shifting customer preferences for contactless driven by the pandemic

The pandemic has led to significant shifts in customer behavior, resulting in an accelerated adoption of digital payments in India. With a focus on minimizing contact and infection risk, customers transitioned to e-commerce and contactless digital payment modes. Over six months following the lockdown imposition in March 2020, there was a notable over 50% increase in monthly transaction volumes across UPI, BBPS, and IMPS. A survey conducted by the BCG Center for Customer Insight during July-August 2020 revealed a substantial decline in cash usage among 50% of customers, with over 60% shifting to UPI and digital wallets compared to pre-COVID times. Moreover, 60% of surveyed customers expressed a strong likelihood of continuing to use digital payments in the future, reflecting a sustained trend in the increased adoption of digital payment methods.

Increased merchant acceptance of digital payments

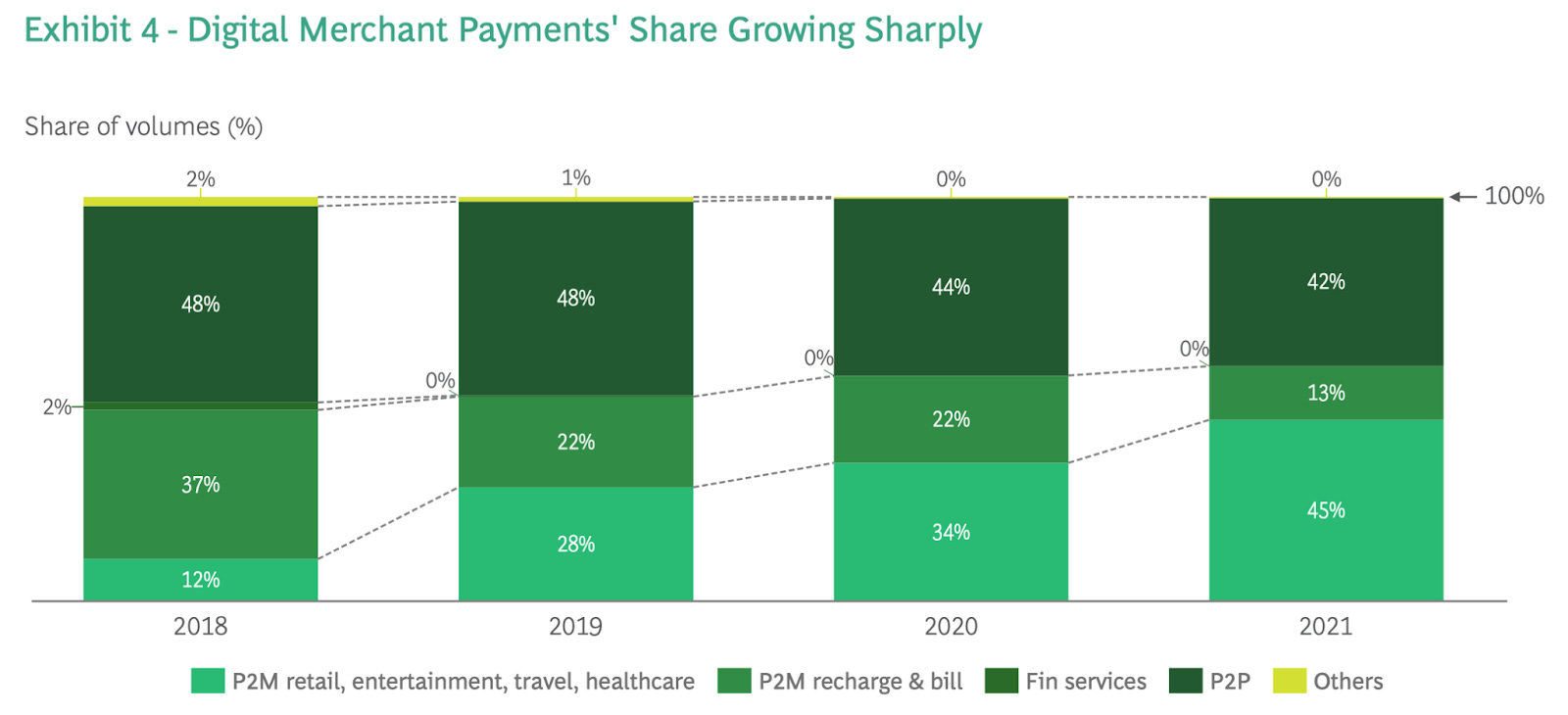

In recent years, there has been a rapid increase in merchant onboarding to digital payments, primarily facilitated by the simplicity, affordability, and convenience of QR codes. Fintech players have played a crucial role in promoting the adoption of QR code payments at merchant points of sale (POS). The acceptance of QR payments has surged, with over 30 million merchants now accepting QR codes—an impressive 12-fold increase from just 2.5 million merchants five years ago. Despite this growth, the total number of POS machines, around 6 million in FY22, has seen limited expansion. QR code acceptance has also extended to 75% of business-to-consumer (B2C) merchants. Consequently, merchant payments have experienced substantial growth, increasing from a 12% share in UPI volumes in 2018 to over 45% in 2021, as indicated by PhonePe Pulse transaction trends data. QR code standardization has played an equally pivotal role to simplify merchant acceptance infrastructure providing uniform user experience for users and merchants alike.

Tech disruptions and enablement by big tech and fintech

India experienced significant startup funding in 2021, with substantial investments totaling $1.4 billion in customer payments players. The digital payments landscape has seen positive disruption with the entry of various new players offering diverse services. Third-party application providers (TPAPs) have played a crucial role in driving payments at scale, while niche players have introduced value-added services such as Buy Now Pay Later (BNPL) options and innovative credit scoring using payments data. Tech giants and leading Indian fintech players have emerged as key drivers of UPI adoption, leveraging user-friendly interfaces, innovative offerings, and the support of an open API ecosystem.

Cash will no longer be king

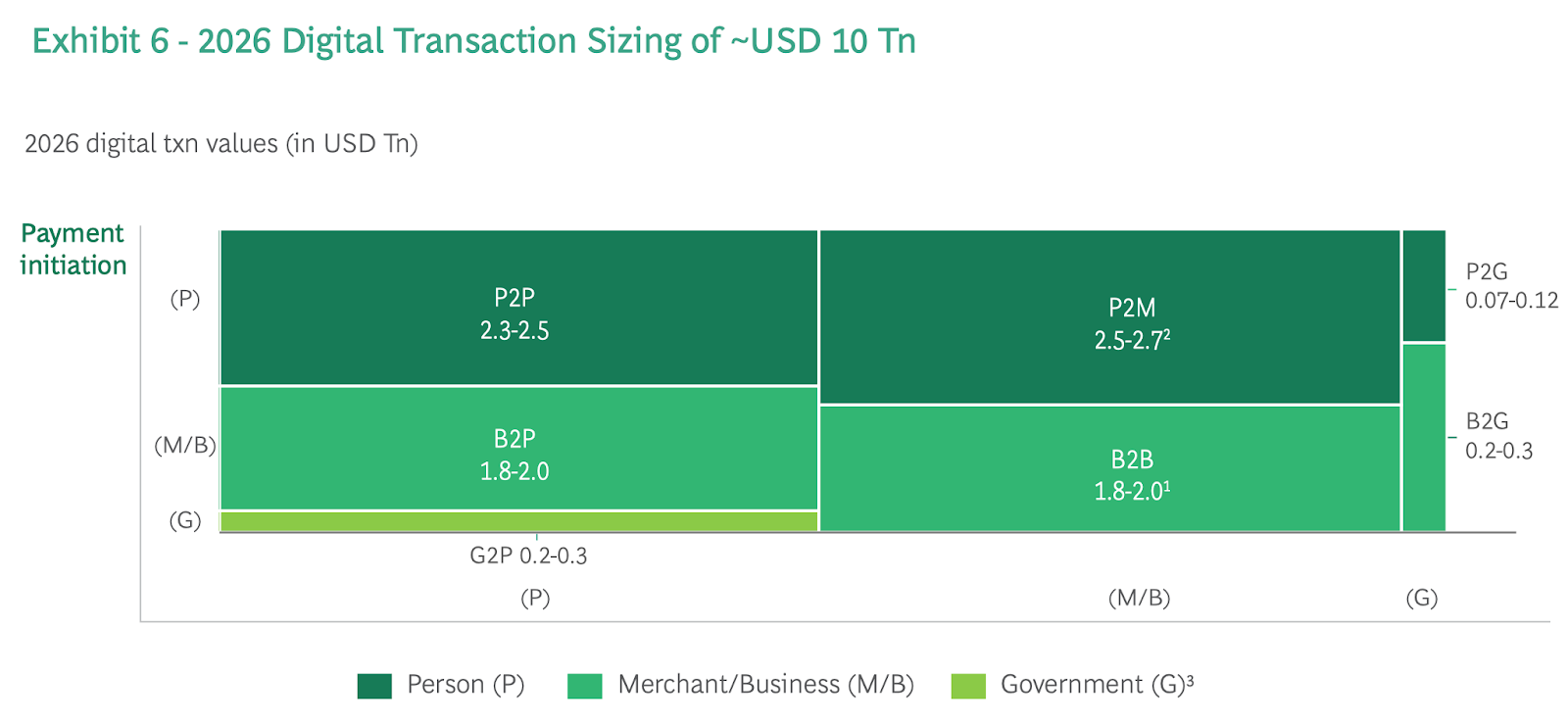

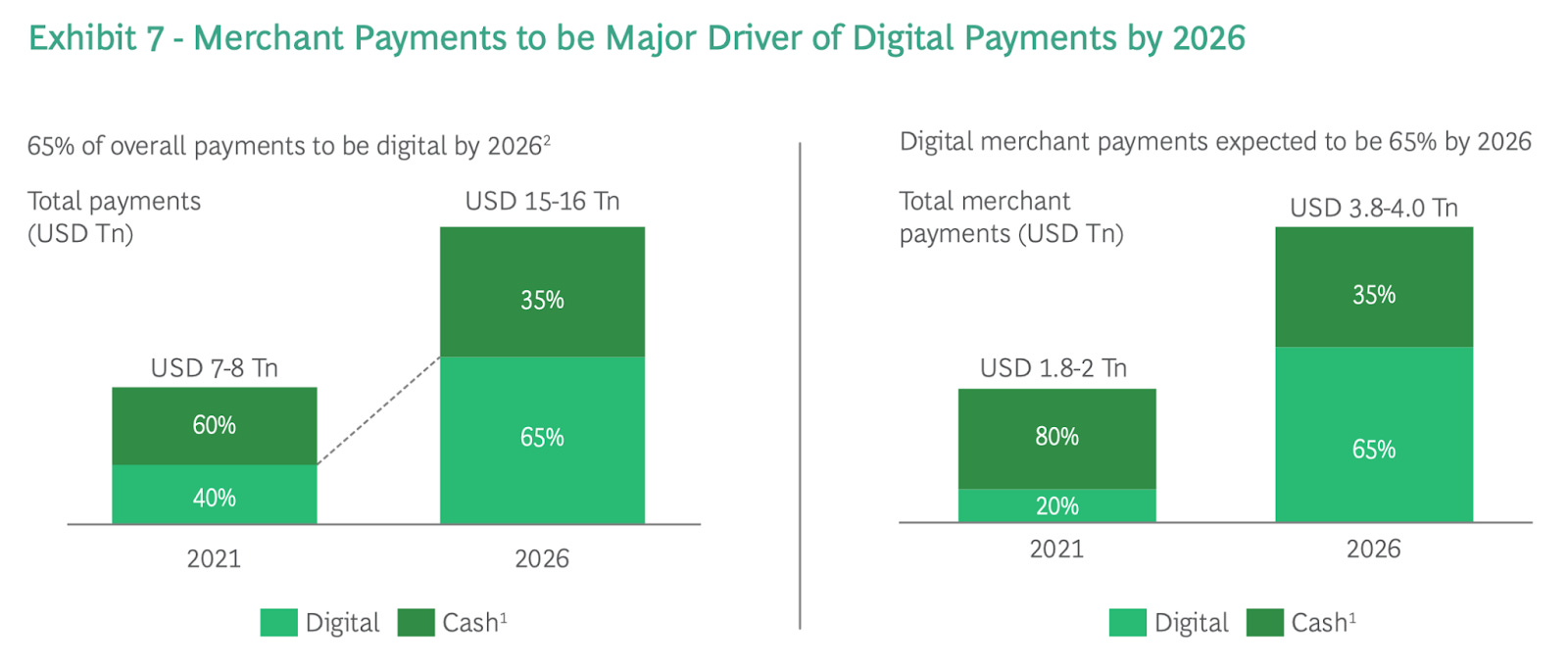

The digital payments market in India is anticipated to more than triple, reaching US$10 trillion by 2026. The projection indicates a shift where 2 out of every 3 payment transactions are expected to be digitized, increasing the digital contribution to payments by value from 40% to about 65%. Merchant payments are anticipated to be a major driver, with an expected increase in digital penetration from 20% to approximately 65% by 2026, translating to a growth from US$0.3-0.4 trillion to US$2.5-2.7 trillion.

The growth in digital payments will be driven primarily by four factors:

1. Expanding merchant acceptance

2. Infrastructure push and set up of a financial services marketplace driving growth in underpenetrated regions

3. Digitized value chains increasing digital payment adoption

4. IoT, 5G and CBDC lending further impetus

• Rapid deployment of QR codes at offline merchants

The offline segment is expected to contribute approximately 75% to all digital merchant payments, primarily driven by the widespread use of QR-based payments at point-of-sale (POS). Currently, around 30 million business-to-consumer (B2C) merchants accept QR code payments at POS, and this number is projected to increase to cover about 40 million merchants. The digitization of merchant payments will be primarily fueled by the offline unorganized segment, with additional contributions from organized offline and online merchant payments, including bill payments and recharges. The cost advantages, coupled with the convenience of QR code installation, are expected to drive merchants to shift from cash to digital payments, despite the absence of a merchant discount rate (MDR) for UPI transactions.

• Greater merchant engagement through integrated POS solutions

To further enhance merchant engagement, tailored solutions addressing specific industry needs, such as Point-of-Sale (POS) terminals integrated with supply chain management, accounts payable and receivable tools, inventory management, and customer relationship management (CRM) tools, can be introduced. These integrated POS solutions would enable merchants to streamline their operations and transactions on a unified platform, automate financial processes, and attract customers through targeted loyalty services. While India has made significant strides in digital payments, there is still untapped potential in Tier 3 cities, rural areas, and beyond. The continuous expansion of payments infrastructure and the evolution of financial service marketplaces present substantial opportunities for growth in these regions.

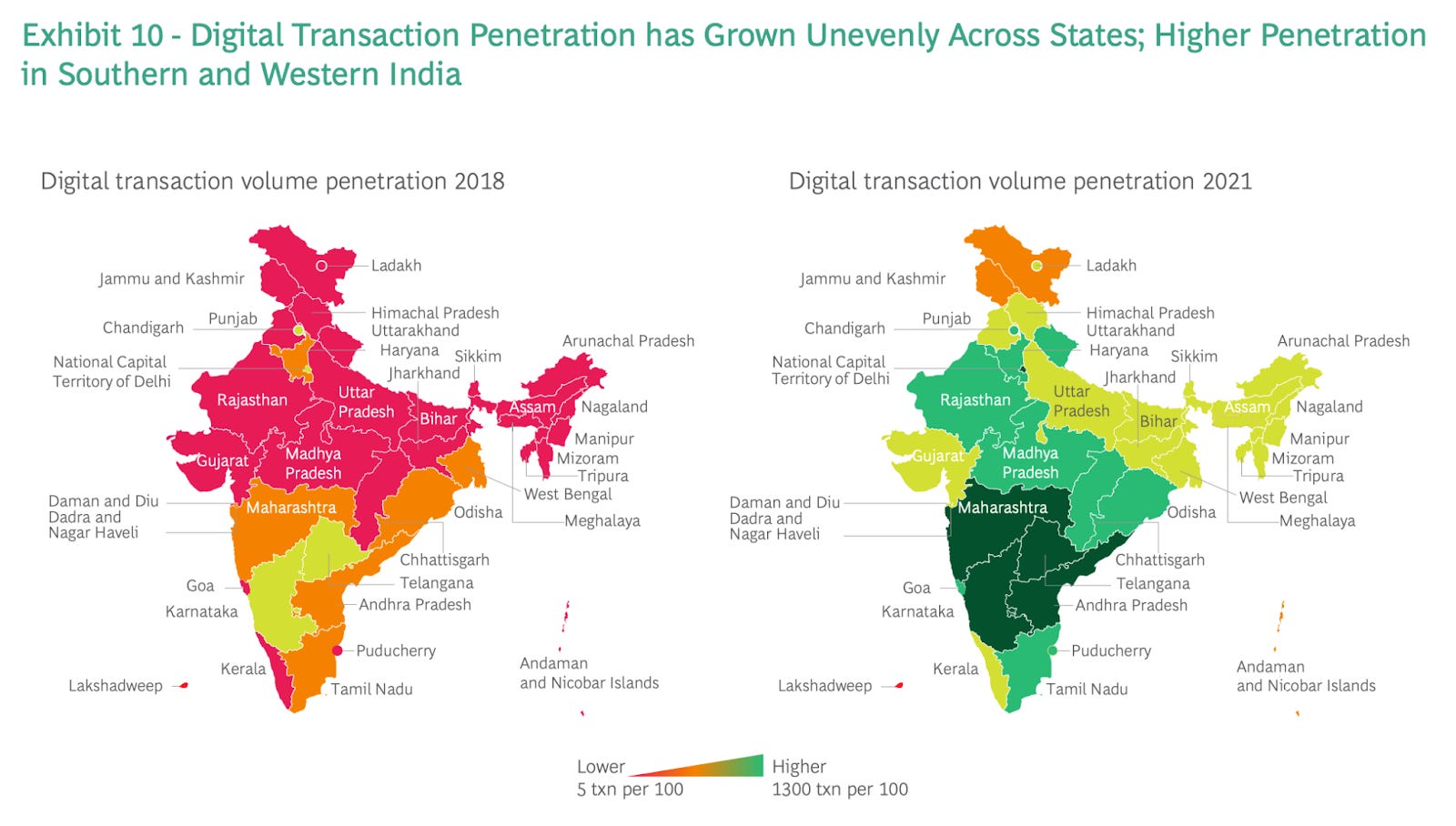

Digital payment penetration is skewed in India

• Building a marketplace crucial to enable participation of rural users

Building a financial services marketplace in underpenetrated regions will be crucial to enable participation of rural customers in financial activities; driven by financial literacy with guidance on getting started and using digital payments.

Through UPI 123Pay, the feature phone user could undertake payments using a pre-defined IVR (Interactive voice response) number, payments via missed call, through app developed for feature phones or proximity sound-based payments.

Digitized value chains increasing digital payments adoption

To enhance financial inclusion in underpenetrated regions, the creation of a financial services marketplace is crucial. This marketplace, as proposed in the 2022 Budget speech, could leverage the extensive network of post offices, connecting them to the core banking system and Digital Banking Units (DBUs) established by the banking ecosystem. This initiative aims to provide a range of banking services tailored for semi-urban and rural areas.

Furthermore, to drive widespread adoption of digital payments, the introduction of innovative instant payment services like UPI 123Pay is essential. UPI 123Pay facilitates payments for feature phone users through methods such as pre-defined IVR (Interactive Voice Response) numbers, payments via missed calls, feature phone apps, or proximity sound-based payments. This approach aims to make digital transactions accessible even to those using basic mobile phones.

• Supply chain digitization for merchants

To encourage small merchants to adopt digital payments and transition away from cash, it is essential to digitize the entire supply chain. The Open Network for Digital Commerce (ONDC) plays a crucial role in this by providing an open network for various aspects of digital trade, aiming to promote digital inclusion among small merchants. ONDC facilitates seamless and cost-effective merchant onboarding to e-commerce platforms, streamlining operations and improving logistical efficiencies.

The implementation of ONDC is expected to benefit online merchants by potentially lowering merchant discount rates through increased competitiveness within the open network. This initiative can also help merchants establish credit histories and reduce customer acquisition costs by accessing users through a unified platform.

Government support in the form of incentives to seller platforms and payment gateways is crucial for the success of such initiatives. Similar to the incentives provided for UPI, government support encourages platforms to offer low-cost payment services to smaller merchants, compensating for the potential loss of revenues due to zero Merchant Discount Rate (MDR) in UPI merchant payments.

Digitization of customer at last mile!

The limited availability of digital spending options hinders the adoption of digital payments, especially in areas with low digital penetration. The key is to integrate digital transactions into customers' daily lives, fostering an environment where digital payments are used for various activities. The success of FASTag in India's toll collections exemplifies the positive impact of digital initiatives, significantly reducing cash handling and promoting electronic toll collection. With 49 million FASTag issued and over 2.4 billion transactions in FY22, it demonstrates the potential for widespread digital payment growth.

Other instances, like the success of BBPS providing accessible bill payment services, highlight the importance of interoperability and diverse payment modes for encouraging digital transactions. Extending this digitization to sectors like rural e-commerce, last-mile deliveries, healthcare, and agriculture services could further accelerate digital adoption. The convergence of technologies such as IoT and 5G, along with the potential introduction of a Central Bank Digital Currency (Digital Rupee), is expected to drive the next generation of payments, offering seamless experiences and addressing security concerns in digital transactions.

Emergence of M-to-M payments

Embedded payments streamline the purchasing process, making transactions seamlessly integrated into various activities. This approach minimizes the time, effort, and manual steps usually required for transaction initiation, authentication, and completion. The most compelling application of IoT-enabled payments is observed in B2B transactions, where payments are seamlessly integrated into core business activities.

In the context of supply chain management, such as inventory restocking and reordering, embedded payment solutions consolidate fragmented processes into a unified functionality. For instance, 5G-enabled smart vending machines in locations like malls or airports can autonomously sense inventory needs, issue restocking orders, and initiate payments on behalf of the company, exemplifying the efficiency of embedded payments in B2B scenarios.

Launch of Digital Rupee

Digital currencies have gained global traction over the past decade, and India is set to join the trend with the anticipated launch of the Digital Rupee. Over 40 countries have explored Central Bank Digital Currencies (CBDCs) to facilitate real-time settlements and enhance transparency. The Digital Rupee, proposed by the Reserve Bank of India (RBI), aims to enable real-time settlement across various use cases, particularly improving cross-border transactions by reducing foreign exchange risk and enhancing B2B payments through decreased counterparty risks. The use of blockchain technology in CBDCs could further diminish settlement risks. Additionally, CBDC transactions offer traceability and transparency, potentially streamlining reversal and refund processes that are currently manual and time-consuming, ultimately improving user experience and trust.

Embedded payments to embedded finance

Seamless payments journey in investment sphere:

In FY21, equity and mutual fund investments in India surged, with active demat accounts doubling to 73 million and the retail investor base growing over 8 times to reach 100 million. Despite this, only 7-8% of the population participates in the stock market, a fraction compared to the USA (55%) and the UK (33%). Currency and deposits dominate savings, but equity and mutual funds are expected to capture 25% of savings by 2025.

The adoption of UPI-based autopay for Systematic Investment Plans (SIP) has played a key role in this growth, offering increased awareness, convenience, and customization. UPI mandate transactions saw a fivefold increase in the last six months, totaling around 32 million in March 2028.

Additionally, UPI IPO mandates have contributed to investment growth, with a threefold increase in the last six months of 2021. The top 5 remitter banks experienced 30-70% growth in IPO volumes processed through UPI, attracting a wider demographic. UPI's simplified process through mobile applications, coupled with incentives for Third-Party Application Providers (TPAPs) to promote subscriptions, has further fueled investment activity.

Integration of payments and lending with advent of BNPL:

Buy-now-pay-later (BNPL) is a key intersection of payments and lending, poised to grow at 35-40% over the next 5 years. Driven by increased consumerism, online spending, and low credit card penetration in India, BNPL's potential is significant. Ecosystems embedding credit within the digital payments journey are rapidly emerging, as seen with Ola's postpaid pay-later option.

In India, two prevalent BNPL variants are deferred payments and check-out financing (EMI). Currently, offline BNPL dominates, capturing 95-98% of the market, with online BNPL expected to hold 40% by FY26.

Enabling greater access to merchant credit

BNPL is gaining popularity among both merchants and customers, offering an integrated model that boosts customer conversion and average order value. Globally, financial institutions leveraging payment data for credit assessment could drive economic formalization, enhance tax compliance, and improve GST collections through digital payments' transparency.

• Credit worthiness increasingly dependent on payments data

The importance of transaction data in credit assessment has increased significantly, rising from approximately 10% to around 50%. This shift is attributed to transaction data providing detailed analytics-based insights into purchases and cash flows. The evolving landscape of credit assessment relies heavily on transaction data, especially with the growth of digitization in person-to-merchant (P2M) payments.

Fintechs better poised to meet the unmet lending demand

Indian financial institutions are increasingly adopting transaction data-driven credit assessment to extend credit access to previously excluded merchants amidst the digital payment shift. The unmet demand in MSME lending, estimated at 35-40% (US$250-260 billion), presents an opportunity. With over 90% of UPI digital transactions led by Third-Party Application Providers (TPAPs), the lending landscape is expected to follow suit, necessitating innovation by traditional banks to compete in this evolving fintech-driven space.

Providers expanding beyond payments:

Payments players are increasingly looking beyond traditional payments to not only offer high margin services but also make the most of lucrative commercial outcomes of the unprecedented digital payment growth in India.

Beyond highly competitive market and regulatory pressure forcing low transaction charges, there are other drivers behind the emergence of super apps like:

1. Lucrative for customers who do not want multiple apps

2. With a super app, merchants only need to integrate with one app to access a large customer base of highly engaged users on a single platform. Global example of Super App: In Indonesia, Gojek evolved as a ridesharing platform and now offers a suite of services, including e-wallet, travel, banking & insurance, food and grocery delivery, e-commerce, and loyalty.

Harness the power of data with personalized offerings:

Payment providers, such as Third-Party Application Providers (TPAPs) and wallets, focus on customer journey curation to enhance user loyalty to digital payments. This involves guiding users through various use cases to establish habits, transitioning them from low spend and low frequency to high spend and high frequency. Gamification of payments and prompts are utilized in curated customer acquisition and engagement journeys.

Additionally, hyper-personalization plays a key role in retention and engagement. Rich payments data is analyzed at an individual level, enabling the provision of personalized services tailored to the specific needs of each customer. This approach drives the offering of targeted services, deals, and incentives, encouraging users to expand their reliance on the app beyond payments alone.

Continued push and support required:

Driving digital payments growth and innovative business models would require support and investments from both the authorities (Government and RBI included) and the payments players.

Simplify onboarding with CKYC

Build customer trust and awareness:

Ensuring data privacy and transparency is crucial for modern communication. Financial institutions should offer accessible platforms for users to manage data consent, and customer education is key to reducing fraud. While current cybersecurity spending by Indian banks is below the global benchmark, there is an expectation of increased spending in the future due to rising cyber threats.

Addressing social engineering and promoting awareness in payment flows is essential to combat fraud. Proactive measures, including mandatory card tokenization, real-time transaction tracking, customer education, fraud reporting integration, multifactor authentication, and default transaction limits for new users, are crucial for fraud mitigation.

Research indicates that these measures not only lower cybersecurity threats but also build trust in financial institutions, ultimately increasing the usage of digital payment services.

Allow sustainable economics for facilitators: Incentives for financial institutions through sustainable MDR would be critical to encourage them to drive merchant acquisition and engagement and digital payments growth. A sustainable MDR is crucial to this pursuit. Introducing an MDR of 0.2-0.3% of the transaction value for small tickets can allow banks, payment players and the overall ecosystem to run sustainable businesses.

Reduce strain on bank infrastructure: The surge in digital transactions is straining bank systems, causing technical declines in UPI transactions. Limited scalability of banking platforms is a key issue. To address this, banks are advised to explore cloud migration, incentivized by infrastructure upgrades. Service quality can be enhanced by reducing core system interactions and managing transactions outside it. UPI Lite, for small offline debit transactions, operates in batch mode, alleviating core banking stress. Authorities may consider setting transaction success rate thresholds for banks.

Strengthen national digital infrastructure: Achieving widespread, affordable internet access is essential to unlocking the full potential of digital payments in underpenetrated regions, fostering trust and improving customer experiences. The advent of 5G is crucial for enabling high-speed, hyperpersonalized payment solutions, including embedded payments on customer handsets, cloud-based solutions, and voice/sound-enabled transactions. 5G speed also enhances fraud monitoring and prevention. However, the rapid transition to a 5G-enabled ecosystem must prioritize security to maintain trust at every stage of the digital payments journey.