Article 20 Summary: How-india-lends-FY22

Report by CRIF

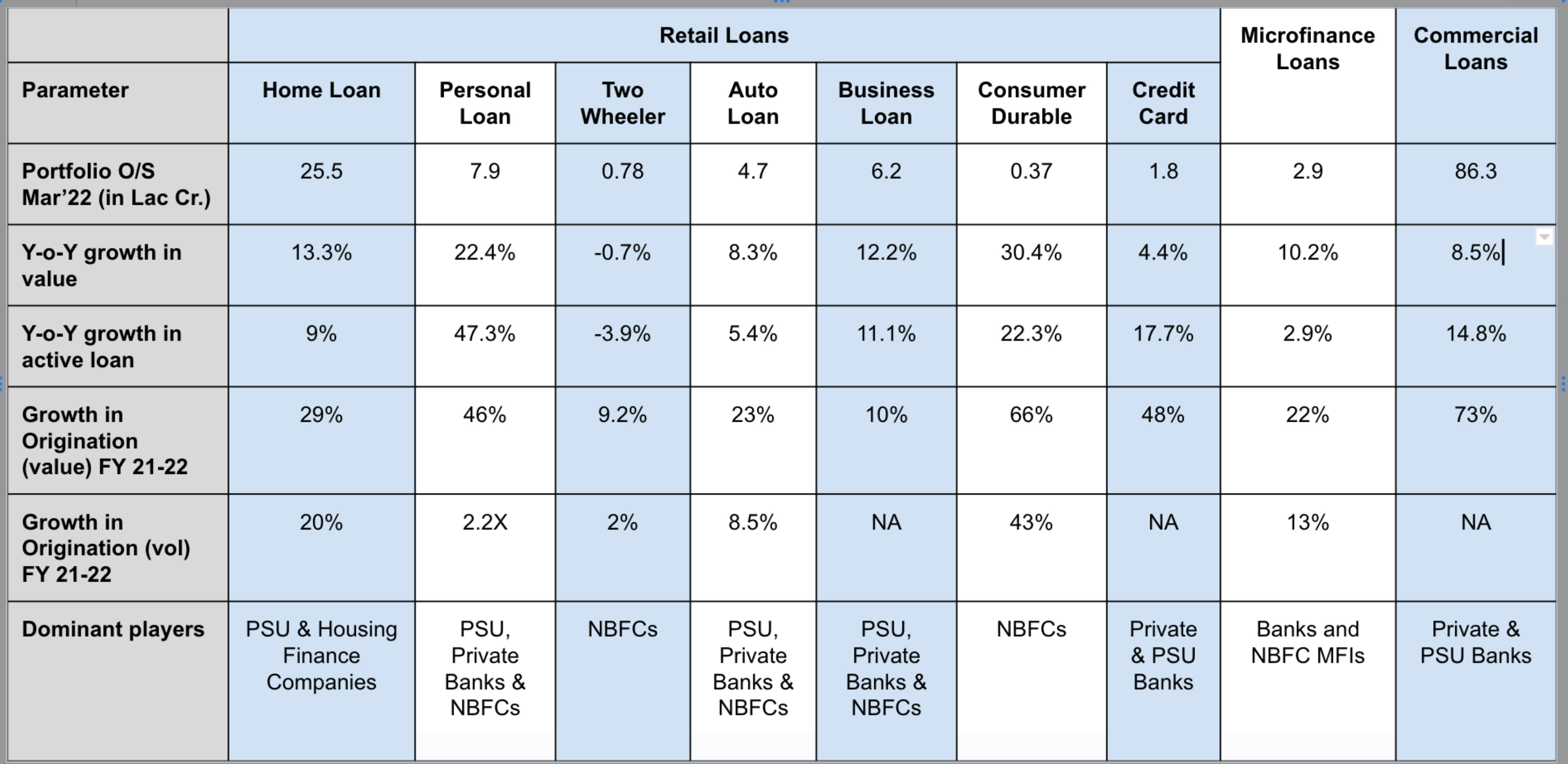

This report provides insights into the lending landscape in India from FY21 to FY22, highlighting the performance of various lending product categories:

Indian lending report

The document compares growth of various loans over the last financial year.

The growth in PL, CD & CC clearly indicates the rising demand for consumer finance.

All loans show a drop in Q1 FY22 due to COVID second wave & recovery from Q2 FY22 onwards.

Home Loans:

7.7% increase in Average Ticket Size (ATS) for Home Loans from Rs.28.4L in FY21 to Rs.30.6L in FY22

Originations share (by value and volume) consistently increased for Public Sector Banks and decreased for Private Banks from Q1 FY22 to Q4 FY22

Personal loans:

There was a 46% growth in originations by value and a 2.2 times growth in originations by volume from FY21 to FY22.

The ATS of personal loans decreased by 33.6%, from Rs.1.25L in FY21 to Rs.83,000 in FY22.

While NBFCs have ATS of Rs.22.7K in FY22, NBFCs specializing in small ticket, small tenure loans have ATS of approx. Rs.7K

Two Wheeler Loans:

Originations dominated by ticket size Rs.50K-75K and Rs. 75K-1L from FY20 onwards

From FY21 to FY22, 8.2% growth in ATS of Private banks from Rs. 74K to 80K, 7.1% growth for NBFCs from Rs.65.8K to 70.5K

Auto Loans:

Originations dominated by ticket size <Rs. 5L and Rs.5 L-10 L. Increase in Originations share (by value) for ticket size Rs>10 L from FY21 to FY22 .

FY21 to FY22, ATS increased by 15.3% for Public Sector Banks from Rs.6.5L to 7.5L, 12.8% for Private Banks from Rs. 7.8L to 8.8L and 9.5% for NBFCs from Rs. 4.2L to 4.6L.

Business Loan:

Originations (by value) dominated by >Rs.50L loans and Rs. 1L - 10L loans, while Originations (by volume) dominated by <Rs.1L loans

FY21 to FY22, ATS increased for Public Sector Banks from Rs. 1.7L to 2.9L and NBFCs from Rs. 3.1L to 5L while declined for Private Banks from Rs. 10.1L to 5.6L.

Consumer Durable Loans:

Non-Banking Financial Companies (NBFCs) dominate the consumer durable loans market both in terms of value and volume.

There has been improvement in the PAR 91-180 (i.e., loans that are 91-180 days past due) from 2.4% to 0.6% from March 2021 to March 2022.

FY21 to FY22, Increase in ATS for Private Banks from Rs. 18.5K to 20.7K and NBFCs from Rs. 18.3K to 21.4K.

Credit Cards:

Private banks have a larger market share than other issuers in both credit card balances and cards in circulation.

The total balances of credit cards in circulation amount to 181.2K Cr, with a 4.4% Y-o-Y growth in value and a 17.7% Y-o-Y growth in volume.

There has been an increase in PAR 90+ (i.e., loans that are 90+ days past due) from March 2021 to March 2022.

Share of New Card Originations of Private Banks increased from 61.2% in FY21 to 71.4% in FY22

Share of New Card Originations of Private Banks reached nearly 80% in Q4 FY22

Microfinance Lending:

Banks have the largest market share in terms of both value (37.7%) and volume (36.3%) of active loans in microfinance.

There has been improvement in PAR 91-180 and PAR 31-90 (i.e., loans that are 31-90 days past due) from March 2021 to March 2022.

7.6% increase in ATS from FY21 to FY22

Originations (by value) dominated by Rs.30K-50K

-Proportion of borrowers having exposure to 4 or more lenders has reduced from 4.4% in Mar’20 to 4.0% in Mar’22.Among major states, proportion of exposure to 4 or more lenders is highest for Tamil Nadu (9.2%) and least for West Bengal (0.8%)

Commercial Loans India Analysis:

The document provides a summary of the commercial loans industry in India for the fiscal year 2022.

The portfolio outstanding value of commercial loans is 86.3 Lakh Cr as of March 2022, with a year-on-year growth of 8.5% by value and 14.8% by volume (active loans).

There has been an improvement in PAR 91-180, decreasing from 1.4% in March 2021 to 1.1% in March 2022.

Private banks and public sector banks dominate the commercial loans market share.

The ATS of loans increased across all lender types from FY21 to FY22.

There has been an increase in the originations share (by value) of MSMEs from 27.2% in FY21 to 38.1% in FY22.

Micro borrower segment continues to dominate originations (by volume) but with a decline in share from 53.7% in FY21 to 46.1% in FY22.