Article 27 Summary: Lending for MSME Bharat- Roadmap

Artcile by NLCI

Summary

The document discusses the challenges and potential solutions for making credit more accessible in society, with a focus on MSMEs and the agricultural sector. It proposes measures to improve the cost, time, and access to credit, as well as enhance risk management. The document also explores trends shaping India's lending industry, including financial inclusion initiatives and the emergence of fintech ecosystems.

It acknowledges the challenges faced by MSMEs and core sectors in accessing credit, such as high interest rates and lengthy loan processing times, and suggests measures to address these issues through technology and simplified loan processes. The document also discusses various aspects of the evolving lending model, such as customer acquisition, credit modeling, disbursal, collection, fraud, and risk management. It suggests using electronic signing, tools like UPI and AEPS for distribution, and integrating risk management with multiple data sources. The solution architecture section outlines the modules and interfaces involved in the lending process.

Let’s get started…

Driving India towards $5 Trillion Economy by 2024-25

The document highlights the poor growth of MSMEs and the agricultural sector, which rely on informal sources for loans.

MSME contributes 30% to GDP, and Govt vision is to take 50% to GDP

Agri contributes to 17% of GDP

The growth in MSME & Agri loans is half as compared to the growth of the retail loans

Following measures have been proposed to handle this:

Improve the cost of credit

Reduce the time to credit

Improve access to credit

Enhance risk management

Improve the cost of credit: The cost of credit ranged between 18-40% IRR in 2019. Aim is to take this to 12-14% IRR by 2024.

Proposed Measures:

Acquisition of borrowers at marketplace like BHIM UPI

Enable single window of EKYC through online onboarding of customer through verification of borrowers and documents

Enable access to data of borrowers for better underwriting through fast track implementation of public credit registry and Account Aggregators

Setup central risk management hub for better view on borrower’s financial health and measures on cash flow based collection

All the above measures are supposed to impact the costs by 15-20%.

Reduce the time to credit: The TAT in 2019 was 20-40 days, and the aim is to take it down to 4hrs-2days by 2024

Proposed Measures:

Simplification of application forms and mechanism for auto fill of forms

Setup single window of borrower’s EKYC ; coupled with Video KYC Unified registration records for MSME ( through GST, NSIC, MCA etc)

Online access to documents such as collaterals, land records, financial information, transactions for automated verification- this alone can reduce TAT by 4-10 days

Automated online underwriting engine with direct access to data sources such as PCR, AA, Surrogate Data etc

Improve access to credit: 20% MSMEs had access to credit in 2019, aim is to take this to 75% by 2024

Proposed Measures:

BHIM type Lending APP/ Integrated with other public or private platforms / marketplaces for better outreach

Strengthen BC Network through MicroATM and integrate Lending platform with BC Infrastructure

Market place or Cash flow enabled pre-eligibility verification & notification to MSME/Farmers for loan availability

Enhance risk management: NPAs in 2019 stood at 7-20%, aim is to take this to <4% NPAs by 2024

Proposed Measures:

Integrated risk management with multiple sources of data for financial and banking information & build. Algorithm for Early Warning Signals which will lead to better monitoring

Strengthen eNACH and more options for eMandate integrated with cash flow model for digital collections leading to better and quicker recovery

Analytical engine to re-baseline collection model in line with cash flow cycle of farmers, MSME to address seasonal, market demands for ease of repayment

Proposed Roadmap:

Integrated Lending Platform: Layer of lending platform through NLCI

India stack Upgrade: enhance usage of e-sign and improve eNACH & eMandate scope Push on digitization of physical records

Viability of Borrowers: API based integration with NBFC AA and GSTN,

Digital Underwriting: Integrate Credit Data point with SMERA & other alternate data sources

Digital customer acquisition: UPI like Mobile App & SDK integrated with partner apps (Banks, NBFCs, MFIs, BCs, RRBs, Fintechs ) to tap customers from marketplace; API led customer acquisition at cash flow source; AEPS infrastructure

Collections & Risk Management: AI enabled forecasting mechanism for better early warning signals

Next Phase of Lending: Overview and Roadmap

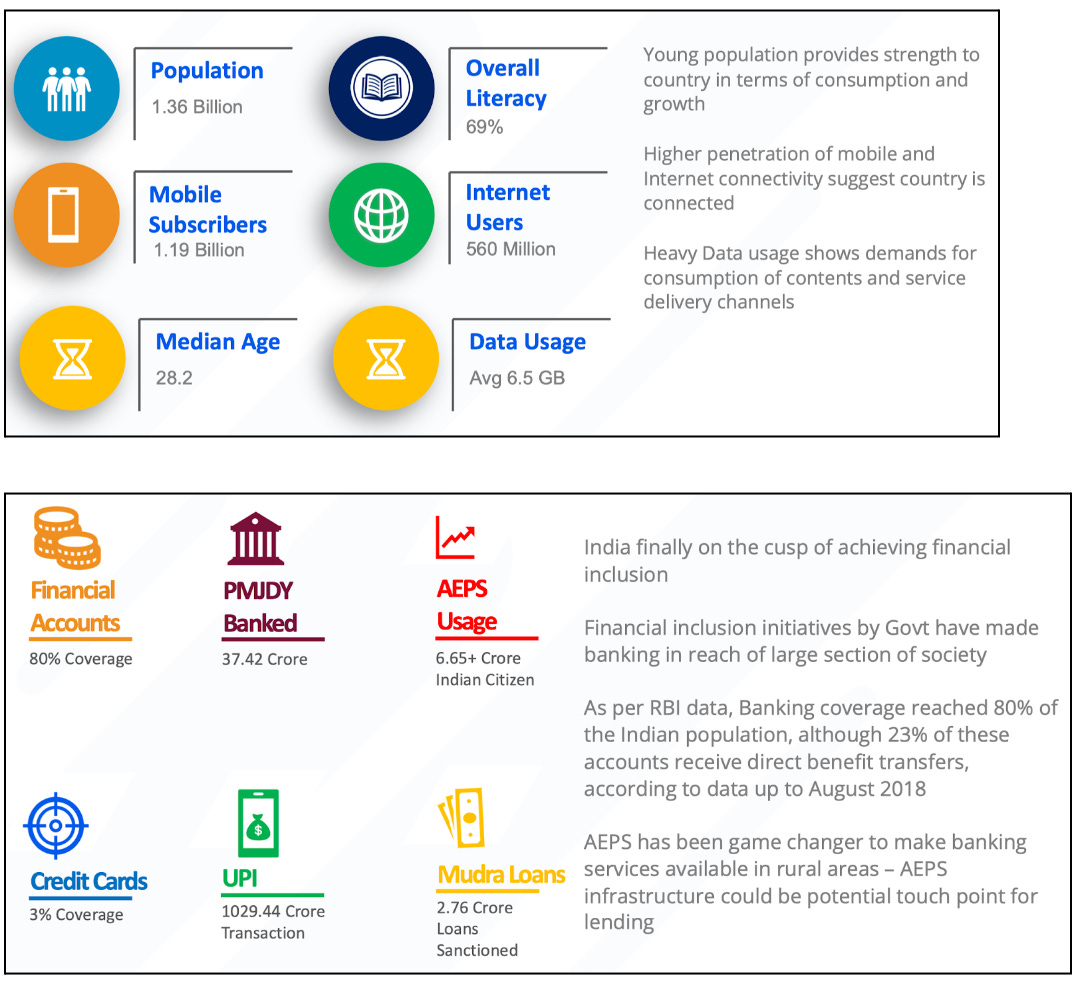

Key Trends Shaping India Lending are:

Demographic factors: Increasing use of smartphones & dropping price of internet

Macroeconomics factors: Cash flow-based lending in trends such as POS, PG enabled lending / Government initiatives like GSTN, Government e-Marketplace, TreDS - GST has pushed registration of MSME* (9.2 Million GST registered) / Schemes like Kisan Credit Card contributed to access to Agri Credit

Financial Inclusion Drive: Push for digital transactions/ Measures to strengthen SIDBI to push for finance to MSME through NBFCs, MFIs and NABARD for agri/ Credit Registration of MSME

Emergence of Fintech Ecosystems: Evolution in technologies such as Open APIs, Mobility, AI/ML driving innovation / Entry of new age Fintechs with ease of transactions / Large Technology players such as Google, Amazon, Flipkart into lending / Increase adoption of digital tools by MSME such as accounting, payments and sales

The document then highlights the major Challenges related to access to credit for MSMEs and core sectors:

Access to credit availability for MSMEs & Core Sectors

Liquidity crunch faced by NBFCs, and high NPAs

Lack of proper risk appraisal mechanism by Banks to provide credit to MSMEs

Banks still major source of credit ( SCBs accounts for 90% of loans to SMEs); and access to Banks a challenge for rural & semi-urban sectors

Absence of a proper legal framework and lack of records relating to agricultural activity

High rate of interest

High costs of customer acquisitions due to outreach efforts esp in remote areas

High onboarding & underwriting costs mainly due to poor credit score or lack of proper risk assessment tools by lenders

High risk factors of business viability of customers, delayed payments, seasonal dependencies ( to cover FLDG)

Cumbersome manual process involve in acquisition and underwriting

High Turn Around Time to Obtain credit from formal sources:

Lack of proper documentation from MSME esp related to financial information or under-reported financials

Traditionally credit team operating from different locations impact of to-and-fro flow of documents and in-person visit to remote areas for physical verification impacts TAT

Cumbersome form filing process

Complexity of Data availability for underwriting process:

Lack of proper records in lending

Very little coverage of any kind of credit score for MSME ( CIBIL SME Score) or SMERA (SME Rating)

No linkages of banking information across banks (Account Aggregator will solve that), and in line with financial information ( Proposed PCR architecture will establish linkage)

Complexity in verification and authentication of borrowers:

Absence of single unique identifier for MSME as Multiple mode of registration of MSMEs such as Udyog Aadhaar, GST, NSIC, Shop & Establishment License etc

Aadhaar only means of KYC for farmers, rural MSMEs

Land records digitization in progress; though same not available for online verification

Challenges related to collections; delay in loan and interest servicing by MSME:

No universal mechanism available for digital collections of loans esp at cash flow level ( eNACH & eMandate limitations)

Absence of universal mechanism for risk management:

Lack of insights on borrower’s business due to sudden changes in external environment like pricing, business model ,regulator and government policy

Lack of insights into Monitoring of use of funds in line of business

Next the document discusses the change in processes across the MSME Loan Value Chain: